2016 – a list of lists regarding the macro investment outlook

2016 – a list of lists regarding the macro investment outlook

Introduction

2015 saw subdued returns for diversified investors as the global economy continued to grow and monetary conditions remained easy, but worries about deflation, plunging commodity prices, fears of an emerging market crisis led by China and uncertainty around the Fed’s first interest rate hike after seven years with near zero interest rates along with continued soft growth in Australia, saw volatile and soft returns from share markets. Balanced super funds had returns of around 5%, which was not disastrous given that returns have averaged 10.1% pa over the last three years, but still disappointing. 2016 has started with many of the same fears seen in 2015. This note provides a summary of key insights on the global economic and investment outlook in simple point form.

Four lessons from 2015

-

Global growth remains fragile and constrained and this is continuing to drive bouts of volatility in investment markets.

-

Deflation still remains a bigger threat than inflation – this is flowing from the secular plunge in commodity prices but also from slower potential economic growth. It reinforces the view that interest rates will remain low for longer.

-

Turn down the noise – despite talk of recessions & crashes, returns from a well-diversified mix of assets were still better than cash or bank deposits.

-

Diversification and active asset allocation are critical – the uneven and volatile return environment (with Australian shares underperforming again) provided a reminder of the benefits of diversification.

Key themes for 2016

-

Global growth of 3% or just above, with the US around 2%, Europe and Japan lagging and China running around 6.5%, but Brazil and Russia still in recession.

-

Scope for a cyclical bounce or at least stabilisation in commodity prices, but in the context of a continuing secular downtrend in response to excess supply.

-

Continuing low inflation on the back of global spare capacity and weak commodity prices, notably oil.

-

Continuing sub-par growth in Australia of around 2.5% for most of the year in response to falling mining investment, the commodity price slump and budget cuts but with the hope of some improvement by year end.

-

Easy monetary conditions with the US very gradually raising rates (two hikes at best, but the risk is one or none), but on going easing in Europe, Japan, China and Australia.

-

A further rise in the $US but at a slower rate than seen over the last two years, with the $A falling to around $US0.60.

-

Modest gains in shares, with global shares outperforming Australian and emerging market shares again.

-

Solid returns from commercial property and infrastructure, but soft gains of around 3% for Australian residential property prices as Sydney and Melbourne slow.

-

Low returns from low yielding cash and bonds.

Key risks for 2016

-

The Fed could prove to be too aggressive in raising rates, and even if it isn’t the fear of this could continue to weigh.

-

The combination of the Fed and low oil prices causing ongoing problems for indebted US energy producers could cause more weakness in credit markets.

-

Political uncertainty could remain a threat in the Eurozone, particularly in relation to Spain (after its messy election) and around populist/extremist parties gaining support.

-

Chinese growth could disappoint with policy uncertainty around Chinese shares and the Renminbi continuing to unnerve investors.

-

Plunging emerging market currencies (and commodity prices) could trigger a default event somewhere in the emerging world on US dollar debt.

-

The loss of national income from lower commodity prices and the continuing unwind in mining investment and a loss of momentum in the housing sector could result in much weaker Australian economic growth.

-

More geopolitical flare ups – eg, South China Sea, tension between Sunni Saudi Arabia & Shia Iran, terrorist threat.

-

Factor X – there is always something from left field. Last year it was China fears.

Five things to watch

-

The Fed – US inflation is likely to be key here.

-

The $US – a continued surge in the $US, particularly via the Chinese Renminbi, will be negative for commodities and emerging currencies raising the risk of an emerging market crisis (eg, a default on US dollar debt).

-

Global business conditions indicators (or PMIs) – these have been slowing for manufacturers but ok for services.

-

Chinese manufacturing conditions PMIs – these need to stabilise around 50.

-

Business confidence and non-mining investment in Australia – these still need to improve.

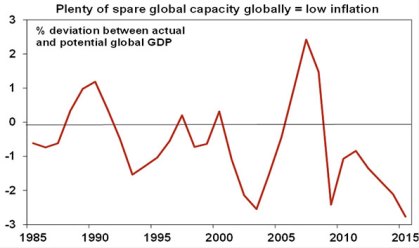

Three reasons why low inflation/deflation is still more likely than a surge in inflation

-

Sub-par global and Australian growth means there is still plenty of spare capacity globally, which means ongoing low pricing power.

Source: IMF, AMP Capital.

-

The fall in commodity prices is still feeding through.

-

The strong $US will import low inflation into the US.

Four reasons why the Fed will likely be very gradual in raising rates (with maybe even no hikes this year)

-

US economic growth remains fragile, particularly manufacturing.

-

Spare capacity remains in the US economy, eg unemployment plus underemployment is still 9.9%.

-

The Fed will be keen to avoid a further strong rise in the $US as it is slowing US growth.

-

Global growth is likely to remain sub-par keeping global inflation & commodity prices soft which impacts US inflation.

Five reasons why the RBA will likely cut rates further

-

The outlook for business investment is still weak.

-

To offset a slowing contribution to growth from housing.

-

Commodity prices are weaker than expected.

-

The $A needs to fall further.

-

To offset the monetary tightening from bank mortgage rate hikes for existing home owners.

Four reasons why Chinese growth will likely come in around 6.5% and not lower

-

The Chinese property market is continuing to rebalance, removing the threat of a property crash.

-

Stimulus measures over the last two years highlight the Government has no tolerance for a collapse in growth.

-

The services sector is taking over from manufacturing.

-

Chinese inflation is very low (with producer prices deflating) indicating still plenty of scope for further monetary easing.

Three reasons why a US/global recession is unlikely

-

We have not seen the normal excesses – massive debt growth, overinvestment or inflation – that normally precede recessions.

-

Nor have we seen the monetary tightening/multiple interest rate hikes that normally precede recessions.

-

Normal lags suggest a big boost to consumers from lower oil prices over the year ahead.

Four reasons Australia won’t have a recession

-

Low interest rates and petrol prices are resulting in big savings to household budgets.

-

The fall in the $A is removing a major drag on growth.

-

Non-mining sectors of the economy beyond just housing are starting to do well: retailing, tourism, higher education and manufacturing is also likely to see a boost.

-

Stronger export volumes (from resource projects) will provide a partial offset to lower commodity prices.

Four reasons why shares are likely to provide decent returns by year end…

-

Share valuations are good, particularly against low bond yields and interest rates.

-

A global recession is unlikely – deep and long bear markets normally require a recession (in the US at least).

-

Monetary conditions are very easy and likely to get easier still as while the Fed may start to tighten other central banks are still easing.

-

There is a lot of pessimism around.

…but three reasons to expect continued volatility

-

Global growth remains fragile.

-

The risk of an emerging market crisis remains high, particularly with China still depreciating the Renminbi versus the $US and commodity prices remaining weak.

-

Shares are not dirt cheap and there is a greater dependence on earnings.

Nine things investors should remember

-

The power of compound returns – saving regularly in growth assets can grow wealth substantially over long periods. Using the “rule of 72” it will take 29 years to double an asset’s value if it returns 2.5% pa (ie 72/2.5) but only 9 years if the asset returns 8% pa.

-

The cycle lives on – markets cycle up and down and we need to allow for it and not get thrown off by rough patches, like the one we are currently going through.

-

Diversify – don’t put all your eggs in one basket and consider active asset allocation to enhance returns/protect against falls.

-

Turn down the noise – the information revolution is making us more jittery and leading to worse investment decisions.

-

Starting point valuations matter – so buy low and sell high. Selling after major falls (like those seen recently) just locks in losses.

-

Remember that while share values can be volatile, the dividend or income stream from a well-diversified portfolio of shares is more stable over time (and now much higher) than the income flow from bank deposits.

-

Avoid the crowd – because at extremes it’s invariably wrong.

-

Focus on investments providing sustainable and decent cash flows – not financial engineering.

-

Accept that it’s a low return world to avoid disappointment – low nominal growth & lower bond yields and earnings yields mean lower long term returns. When inflation is 2.5% an 8% return is pretty good.

AMP Capital Markets 21st January 2016

About the Author

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist at AMP Capital is responsible for AMP Capital’s diversified investment funds. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.