New rules to benefit those downsizing for retirement

New rules to benefit those downsizing for retirement

Downsizers will be able to top up their super with the proceeds from the sale of their main residence from July 2018.

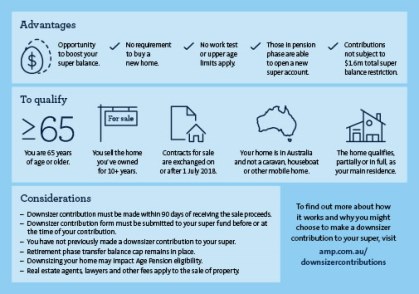

From 1 July 2018, Australians aged 65 and over who are downsizing for retirement will be able to contribute the proceeds from the sale of their main residence (up to $300,000) into super1.

We take a look at what this could mean for you, bearing in mind that like with all important financial decisions, it’s a good idea to get financial advice before deciding what’s right for you.

Super benefits for downsizers

Currently, people aged between 65 and 75 who want to make voluntary super contributions must satisfy a work test, while people over 75 are generally unable to contribute to their super.

From 1 July 2018 that will change. People aged 65 and over will be able to make an after-tax contribution to their super of up to $300,000 using the proceeds from the sale of their main residence – regardless of their work status, superannuation balance, or contribution history.

For couples, both spouses will be able to take advantage of this opportunity, which means up to $600,000 per couple can be contributed toward super.

How does it work?

Proceeds from the sale of your main residence that are contributed into super as part of this initiative can be made in addition to any other before-tax or after-tax contributions you’re eligible to make.

The government said the aim is to encourage older Australians, where appropriate, to free up homes that no longer meet their needs and make room for younger growing families2.

To qualify, the contracts for sale must be exchanged on or after 1 July 2018. The property that’s sold also needs to have been your (or your spouse’s) main place of residence at some point in time, and you need to have owned the home for at least 10 years.

‘Downsizing’ contributions are not tax deductible and can be made regardless of super caps and restrictions that otherwise apply when making super contributions. The property that’s sold must also be in Australia and excludes caravans, mobile homes and houseboats.

Things to note

No special Centrelink means test exemptions apply to the downsizing contribution. Due to this, there may be means testing implications as a result of downsizing, which need to be considered.

Meanwhile, additional rules may apply to your situation, so make sure you do your research before making any decisions.

Also note, , Downsizer Contribution Form from the Australian Taxation Office (ATO) will need to be provided when making, or prior to making, this type of contribution. These forms will be available from 1 July 2018.

Check out this infographic below for a snapshot of some of the advantages and considerations.

Like with most things, when you’re making a big financial decision, which could have implications, it’s worth doing your research . For further assistance please contact us on |PHONE|

Important

This article provides general information and hasn’t taken your circumstances into account. It’s important to consider your particular circumstances before deciding what’s right for you. Although the information is from sources considered reliable, we do not guarantee that it is accurate or complete. You should not rely upon it and should seek qualified advice before making any investment decision. Except where liability under any statute cannot be excluded, we do not accept any liability (whether under contract, tort or otherwise) for any resulting loss or damage of the reader or any other person.